01 · Core Question

Can inherited stories about risk shape the price of credit?

The paper links European syndicated loan contracts to measures of risk-related folklore in the cultural background of lead lenders. The central hypothesis is that cultural narratives may enter credit pricing as soft information, especially when stories emphasize failure after challenge or competition.

What is being explained?

Loan spreads over floating-rate benchmarks, measured at the loan level and modeled with detailed loan, borrower, lender, regional, country, industry, and year controls.

02 · From Tale To Variable

Folklore is converted into measurable cultural exposure.

The empirical design uses the cross-cultural folklore measures of Michalopoulos and Xue (2021), based on Berezkin's catalogue of oral traditions. A motif is a recurrent narrative element: a plot, character, symbolic image, or episode shared across traditions.

Traditional storiesOral traditions collected across cultural societies.

MotifsRecurring narrative elements become the unit of analysis.

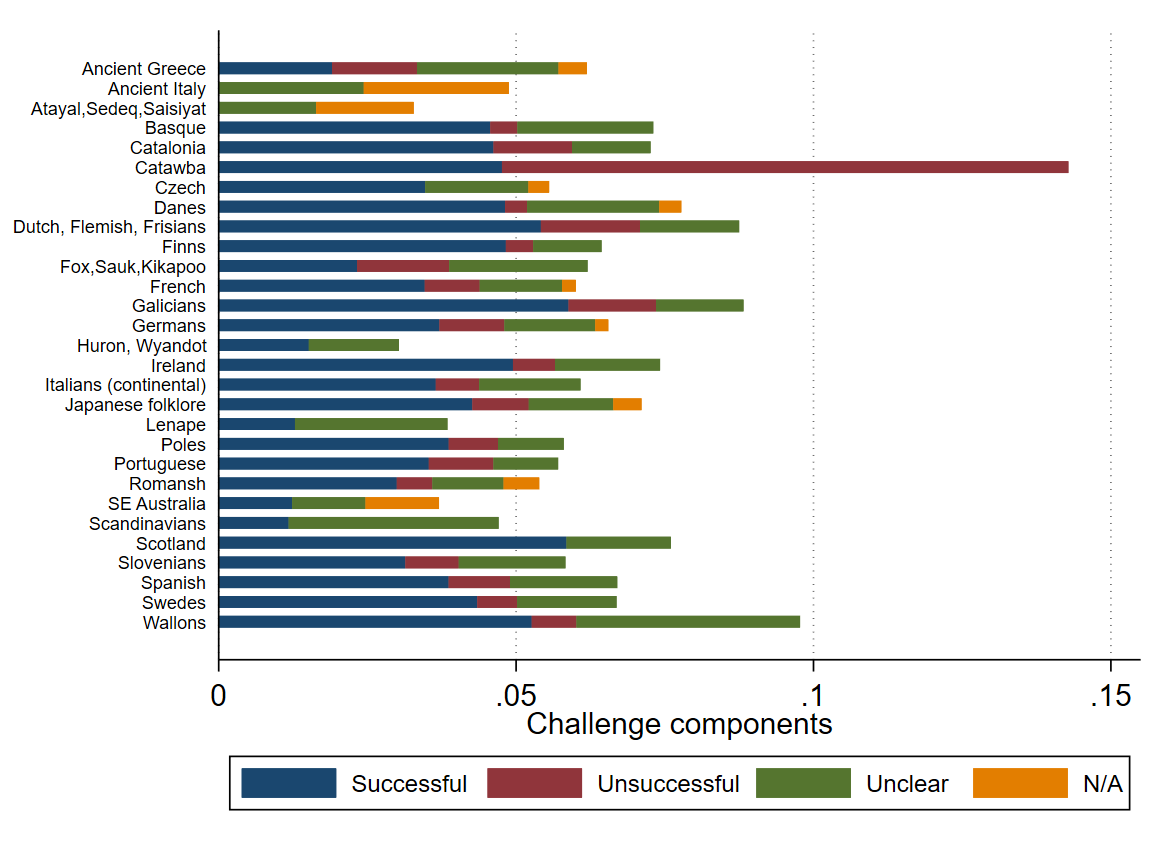

ChallengeMotifs related to challenge, competition, or risky action are identified.

OutcomeChallenge motifs are classified as successful, unsuccessful, unclear, or not applicable.

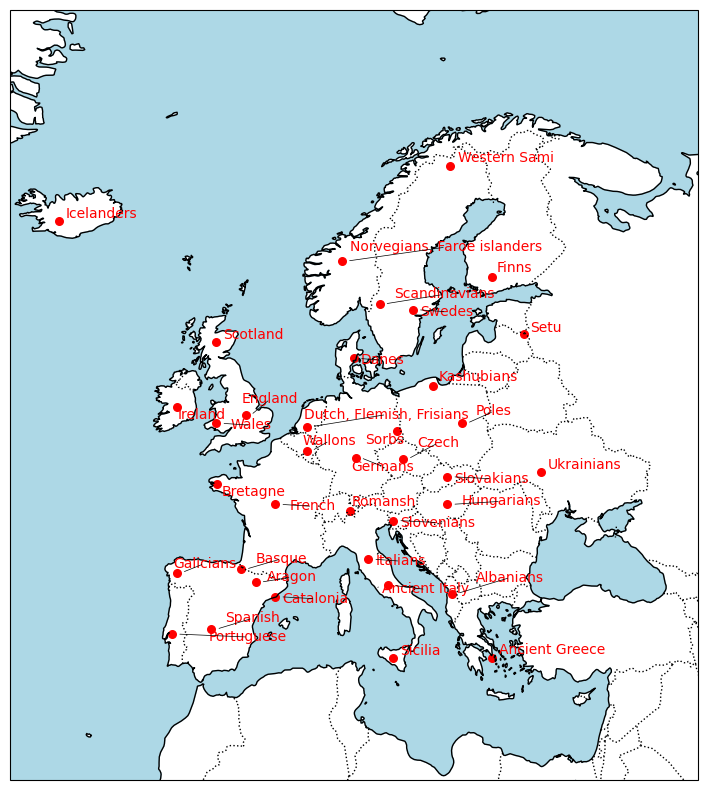

Berezkin groupMotif shares are aggregated at the folklore group level.

Lead lenderThe lead bank's headquarters location is linked to the nearest folklore group.

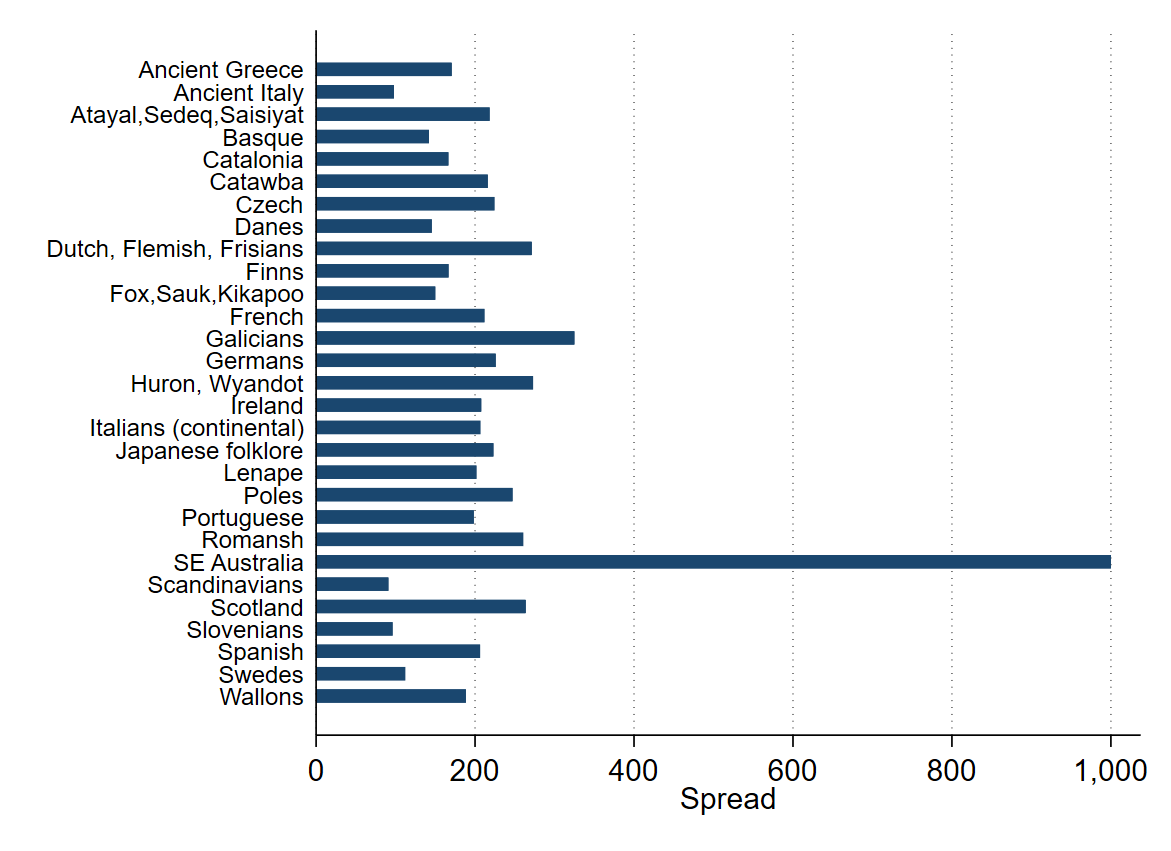

03 · Folklore Groups

Challenge stories vary substantially across cultural groups.

The key explanatory variables are not country dummies in disguise. They vary at the folklore-group level, often below the country level, and distinguish the prevalence and outcome of challenge-related motifs.

04 · Main Evidence

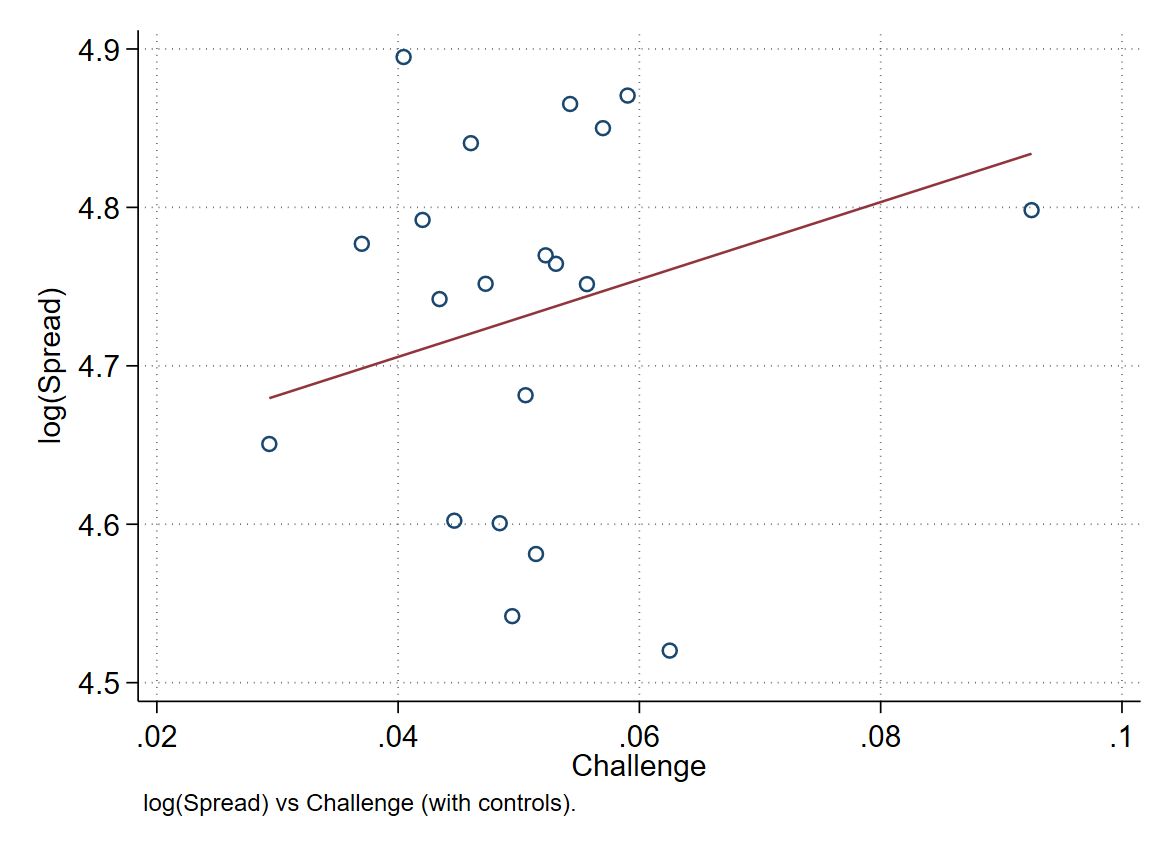

The pricing result is driven by cautionary challenge stories.

+

Challenge motifs

Lead-lender folklore with more challenge-related motifs is associated with higher loan spreads in richer specifications.

+

Unsuccessful outcomes

Failure in challenge narratives carries the pricing effect more clearly than the overall challenge measure.

0

Successful outcomes

Stories where risk-taking succeeds do not show the same spread-increasing effect.

+22.86 bps

Economic magnitude

One standard-deviation increase in relatively unsuccessful motifs corresponds to about 10.5% of the mean spread.

05 · Robustness

The result is checked against alternative explanations.

The paper tests whether the folklore result survives richer cultural, geographic, and econometric controls. The aim is to separate the folklore channel from broader country culture and regional development differences.

Alternative culture

Controls include Hofstede dimensions, religion, trust, and corruption measures. The main folklore variables remain economically meaningful.

Instrumental variables

The IV strategy uses neighboring folklore within a 225 km radius to capture cultural diffusion while limiting direct current-credit channels.

Fixed effects

Additional fixed effects absorb time, industry, borrower-country, and lender-country variation across specifications.

Heterogeneity

Effects are stronger among stronger banks and stronger firms, consistent with folklore complementing, not replacing, hard information.

06 · Open Access Article

Read the paper from the companion page.

The article remains anchored by the journal DOI, while the embedded PDF gives visitors a low-friction way to inspect the argument, tables, and figures without leaving the companion site.

Embedded local PDF reader. Browser support can vary, so the DOI link remains the canonical access point.

Open DOI

07 · Reference And Access

Paper, citation, and reuse note.

This page is a companion to the published article. Numerical claims are drawn from the paper and project figures; readers should cite the article for formal methods and results.

Article: Godlewski, C. and Weill, L. (2026). Tales that cost: Folklore and bank loan spreads. International Review of Financial Analysis, 111, 105100.

DOI: 10.1016/j.irfa.2026.105100

@article{GodlewskiWeill2026TalesThatCost,

title = {Tales that cost: Folklore and bank loan spreads},

author = {Godlewski, Christophe and Weill, Laurent},

journal = {International Review of Financial Analysis},

volume = {111},

pages = {105100},

year = {2026},

doi = {10.1016/j.irfa.2026.105100}

}